2010 PERSONAL TAX CREDITS RETURN TD1

2010 PERSONAL TAX CREDITS RETURN TD1

2010 PERSONAL TAX CREDITS RETURN TD1

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

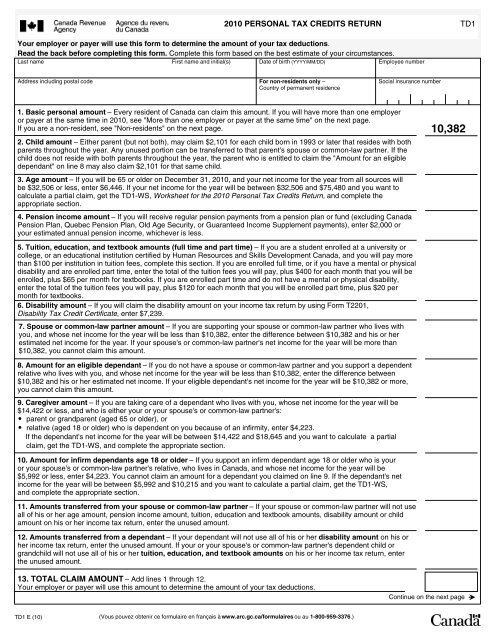

<strong>2010</strong> <strong>PERSONAL</strong> <strong>TAX</strong> <strong>CREDITS</strong> <strong>RETURN</strong> <strong>TD1</strong>Your employer or payer will use this form to determine the amount of your tax deductions.Read the back before completing this form. Complete this form based on the best estimate of your circumstances.Last name First name and initial(s) Date of birth (YYYY/MM/DD)Employee numberAddress including postal code For non-residents only –Country of permanent residenceSocial insurance number1. Basic personal amount – Every resident of Canada can claim this amount. If you will have more than one employeror payer at the same time in <strong>2010</strong>, see "More than one employer or payer at the same time" on the next page.If you are a non-resident, see "Non-residents" on the next page.2. Child amount – Either parent (but not both), may claim $2,101 for each child born in 1993 or later that resides with bothparents throughout the year. Any unused portion can be transferred to that parent's spouse or common-law partner. If thechild does not reside with both parents throughout the year, the parent who is entitled to claim the "Amount for an eligibledependant" on line 8 may also claim $2,101 for that same child.3. Age amount – If you will be 65 or older on December 31, <strong>2010</strong>, and your net income for the year from all sources willbe $32,506 or less, enter $6,446. If your net income for the year will be between $32,506 and $75,480 and you want tocalculate a partial claim, get the <strong>TD1</strong>-WS, Worksheet for the <strong>2010</strong> Personal Tax Credits Return, and complete theappropriate section.4. Pension income amount – If you will receive regular pension payments from a pension plan or fund (excluding CanadaPension Plan, Quebec Pension Plan, Old Age Security, or Guaranteed Income Supplement payments), enter $2,000 oryour estimated annual pension income, whichever is less.10,3825. Tuition, education, and textbook amounts (full time and part time) – If you are a student enrolled at a university orcollege, or an educational institution certified by Human Resources and Skills Development Canada, and you will pay morethan $100 per institution in tuition fees, complete this section. If you are enrolled full time, or if you have a mental or physicaldisability and are enrolled part time, enter the total of the tuition fees you will pay, plus $400 for each month that you will beenrolled, plus $65 per month for textbooks. If you are enrolled part time and do not have a mental or physical disability,enter the total of the tuition fees you will pay, plus $120 for each month that you will be enrolled part time, plus $20 permonth for textbooks.6. Disability amount – If you will claim the disability amount on your income tax return by using Form T2201,Disability Tax Credit Certificate, enter $7,239.7. Spouse or common-law partner amount – If you are supporting your spouse or common-law partner who lives withyou, and whose net income for the year will be less than $10,382, enter the difference between $10,382 and his or herestimated net income for the year. If your spouse's or common-law partner's net income for the year will be more than$10,382, you cannot claim this amount.8. Amount for an eligible dependant – If you do not have a spouse or common-law partner and you support a dependentrelative who lives with you, and whose net income for the year will be less than $10,382, enter the difference between$10,382 and his or her estimated net income. If your eligible dependant's net income for the year will be $10,382 or more,you cannot claim this amount.9. Caregiver amount – If you are taking care of a dependant who lives with you, whose net income for the year will be$14,422 or less, and who is either your or your spouse's or common-law partner's: parent or grandparent (aged 65 or older), or relative (aged 18 or older) who is dependent on you because of an infirmity, enter $4,223.If the dependant's net income for the year will be between $14,422 and $18,645 and you want to calculate a partialclaim, get the <strong>TD1</strong>-WS, and complete the appropriate section.10. Amount for infirm dependants age 18 or older – If you support an infirm dependant age 18 or older who is youror your spouse's or common-law partner's relative, who lives in Canada, and whose net income for the year will be$5,992 or less, enter $4,223. You cannot claim an amount for a dependant you claimed on line 9. If the dependant's netincome for the year will be between $5,992 and $10,215 and you want to calculate a partial claim, get the <strong>TD1</strong>-WS,and complete the appropriate section.11. Amounts transferred from your spouse or common-law partner – If your spouse or common-law partner will not useall of his or her age amount, pension income amount, tuition, education and textbook amounts, disability amount or childamount on his or her income tax return, enter the unused amount.12. Amounts transferred from a dependant – If your dependant will not use all of his or her disability amount on his orher income tax return, enter the unused amount. If your or your spouse's or common-law partner's dependent child orgrandchild will not use all of his or her tuition, education, and textbook amounts on his or her income tax return, enterthe unused amount.13. TOTAL CLAIM AMOUNT – Add lines 1 through 12.Your employer or payer will use this amount to determine the amount of your tax deductions.Continue on the next page<strong>TD1</strong> E (10)(Vous pouvez obtenir ce formulaire en français à www.arc.gc.ca/formulaires ou au 1-800-959-3376.)

Completing Form <strong>TD1</strong>Complete this form only if: you have a new employer or payer and you will receive salary, wages, commissions, pensions,Employment Insurance benefits, or any other remuneration; you want to change amounts you previously claimed (such as when the number of your eligible dependants has changed); you want to claim the deduction for living in a prescribed zone; or you want to increase the amount of tax deducted at source.Sign and date it and give it to your employer or payer.If you do not complete a <strong>TD1</strong> form, your new employer or payer will deduct taxes after allowing the basic personal amount only.More than one employer or payer at the same timeIf you have more than one employer or payer at the same time and you have already claimed personal tax credit amounts on another<strong>TD1</strong> form, you cannot claim them again. If your total income from all sources will be more than the personal tax credits you claimedon another <strong>TD1</strong> form, check this box, enter "0" on line 13 on the front page and do not complete lines 2 to 12.Total income less than total claim amountCheck this box if your total income for the year from all employers and payers will be less than your total claim amount on line 13. Thenyour employer or payer will not deduct tax from your earnings.Non-residentsAre you a non-resident of Canada who will include 90% or more of your world income when determining your taxable income earned in Canadain <strong>2010</strong>? If you are unsure of your residency status, call the International Tax Services Office at 1-800-267-5177. If yes, complete the previous page. If no, check the box, enter "0" on line 13 and do not complete lines 2 to 12, as you are not entitled to the personal tax credits.Provincial or territorial personal tax credits returnIf your claim amount on line 13 is more than $10,382, you also have to complete a provincial or territorial personal tax credit return.If you are an employee, use the <strong>TD1</strong> form for your province or territory of employment. If you are a pensioner, use the <strong>TD1</strong> form for yourprovince or territory of residence. Your employer or payer will use both this federal form and your most recent provincial or territorial<strong>TD1</strong> form to determine the amount of your tax deductions.If you are claiming the basic personal amount only (your claim amount on line 13 is $10,382), your employer or payer will deduct provincialor territorial taxes after allowing the provincial or territorial basic personal amount.Note: If you are a Saskatchewan resident supporting children under 18 at any time during <strong>2010</strong>, you may be able to claim thechild amount on Form <strong>TD1</strong>SK, <strong>2010</strong> Saskatchewan Personal Tax Credits Return. Therefore, you may want to complete Form <strong>TD1</strong>SKeven if you are only claiming the basic personal amount on this form.Deduction for living in a prescribed zoneIf you live in the Northwest Territories, Nunavut, Yukon, or another prescribed northern zone for more than six months in a row beginningor ending in <strong>2010</strong>, you can claim: $8.25 for each day that you live in the prescribed northern zone, or $16.50 for each day that you live in the prescribed northern zone if, during that time, you live in a dwellingthat you maintain, and you are the only person living in that dwelling who is claiming this deduction.Employees living in a prescribed intermediate zone can claim 50% of the total of the above amounts.For more information, get Form T2222, Northern Residents Deductions, and the Publication T4039,Northern Residents Deductions – Places in Prescribed Zones.Additional tax to be deductedYou may want to have more tax deducted from each payment, especially if you receive other income, includingnon-employment income such as CPP or QPP benefits, or Old Age Security pension. By doing this, you may nothave to pay as much tax when you file your income tax return. To choose this option, state the amount of additionaltax you want to have deducted from each payment. To change this deduction later, complete a new Form <strong>TD1</strong>.Reduction in tax deductionsYou can ask to have less tax deducted if on your income tax return you are eligible for deductions or non-refundable tax credits that are notlisted on this form (for example, periodic contributions to a Registered Retirement Savings Plan (RRSP), child care or employment expenses,and charitable donations). To make this request, complete Form T1213, Request to Reduce Tax Deductions at Source, to get a letter ofauthority from your tax services office. Give the letter of authority to your employer or payer. You do not need a letter of authority if youremployer deducts RRSP contributions from your salary.CertificationI certify that the information given in this return is, to the best of my knowledge, correct and complete.$$SignatureIt is a serious offence to make a false return.Date